Summary

- Automotive loans of every kind are on a downward pattern in approvals, with a concurrent enhance in rates of interest

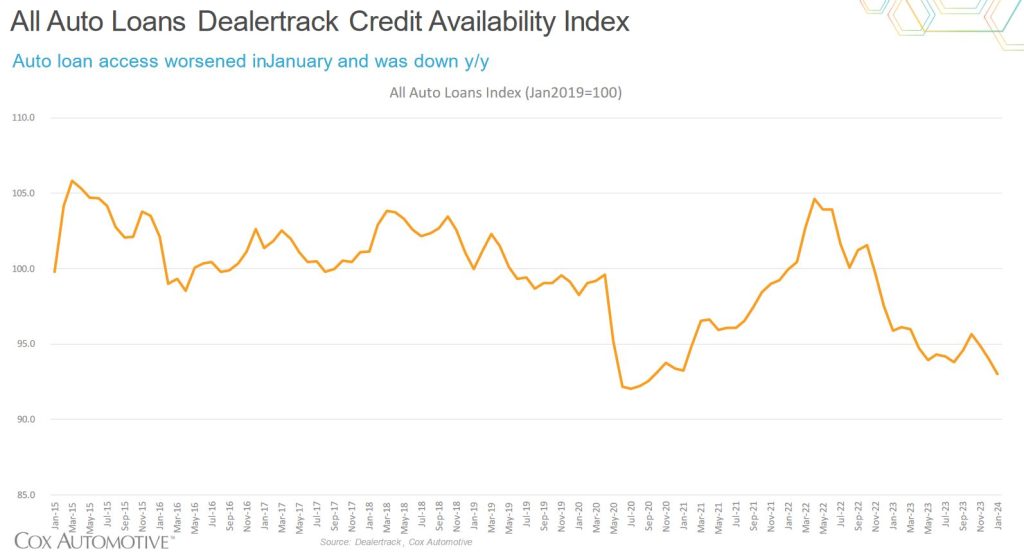

- The auto mortgage availability index has hit its lowest level in 5 years in January 2024 at 93%, in comparison with a baseline January 2019 100%

- Analysis of obtainable date exhibits that there are 4 main components driving this: Credit availability shifting in opposition to customers, approval charges lowering total, time period lengths shortening with 72 month phrases seeing the bottom approvals, and the tightening of different mortgage channels

- From the info, we imagine there are a number of choices that may get a shopper a automobile this yr, however all embrace some type of danger or acceptance of less-than-desirable rates of interest

- Our evaluation additionally exhibits that the pattern would possibly proceed downward for a good portion of 2024, so it will not be value shopping for this yr, new or used.

In the ever-changing panorama of automotive financing, entry to credit score performs a pivotal function in each driving car gross sales via to signing on presents, in addition to shaping total shopper conduct. It just isn’t understating the truth that securing auto credit score may be the make-or-break a part of any sale.

The January 2024 Dealertrack Credit Availability Index (CAI), as reported by Cox Automotive, supplies an in-depth overview of the state of auto credit score availability within the United States. The newest findings reveal a regarding pattern of worsening credit score availability, shedding gentle on the challenges confronted by each customers and business stakeholders.

Year-to-Year Differences

Comparing knowledge from January 2023 to January 2024, the Dealertrack CAI report highlights a notable decline in auto credit score availability. This decline is mirrored via a number of metrics, together with total credit score approval charge and the share of prime and subprime debtors.

That year-over-year credit score approval charge has decreased by a big 3%, signaling a tightening of credit score requirements by lenders. This, regardless of a recovering native financial system within the USA and commerce between the US and Canada normalizing near pre-pandemic ranges.

Additionally, there was a shift within the composition of debtors, with a lower in prime debtors and a rise in subprime debtors, including additional pressure to the lending market. This has mixed to trigger the auto mortgage index to hit its lowest level since August 2020, coming in a full share level under that index.

Analysis

The decline in auto credit score availability noticed within the January 2024 Dealertrack CAI report warrants a better examination of the underlying components which are driving the pattern. Several components could also be contributing to the tightening of credit score requirements by lenders:

- Credit Availability Factors Moving Against Consumers: In January, yield spreads widened on common by 15 foundation factors (BPs), the fast impact of which was rising charges on auto loans. Comparatively, the 5-year US treasury charge decreased by 2 BPs, driving the yield unfold even wider.

- Approval Rates Decreasing Overall: The auto credit score approval charge dropped 8 BPs in January 2024 alone, a 1.6% lower in comparison with January 2023. Subprime shares additionally decreased to 11.2% in January 2024 in comparison with 11.4% in December 2023, regardless of the shares being up 0.6% year-over-year in comparison with December 2022.

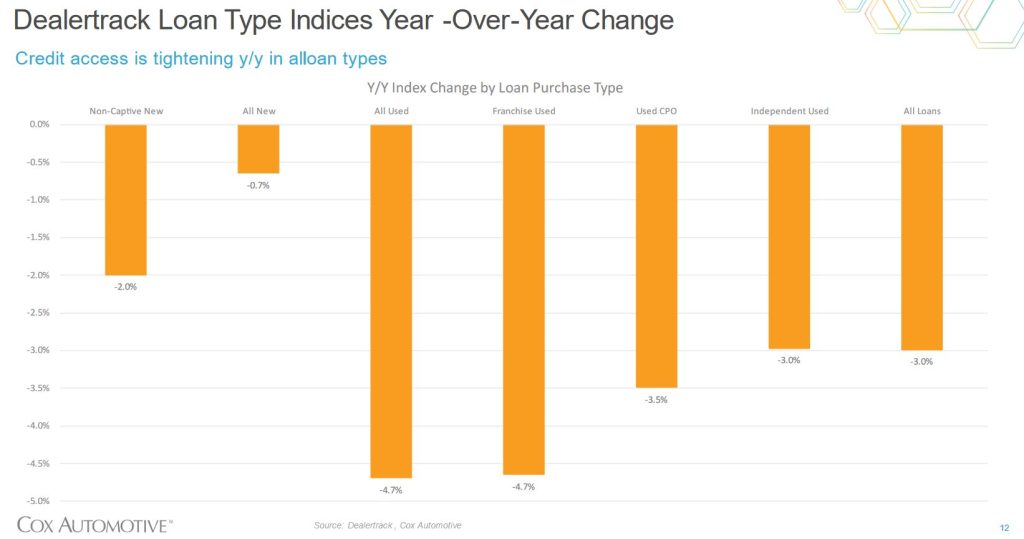

- Term Lengths Decreasing: To mitigate danger, auto credit score lenders decreased the quantity of approvals on long run loans, specifically the 60 and 72 month phrases. The share of loans in January decreased by 2 BPs, leading to a 1.8% lower yr to yr

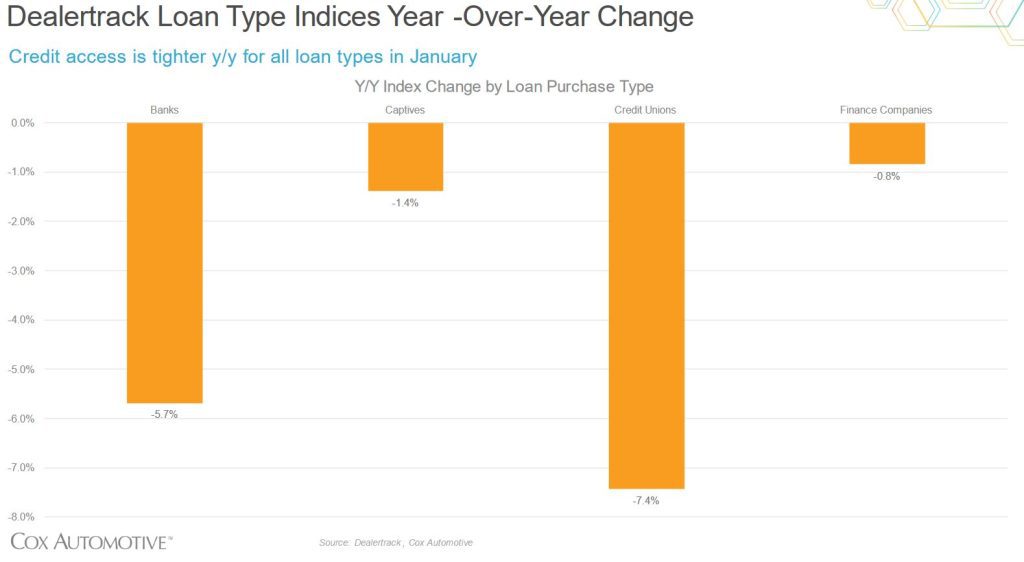

- All Loan Channels Tightening Approvals: It’s not simply major auto credit score lenders feeling the strain. Banks and impartial credit score unions tightened essentially the most, proscribing entry to financing via alternate channels. In a year-to-year comparability, all credit score sorts noticed a big shift in approval charges, typically by as 5.7% for banks and seven.4% for credit score unions.

Overall Conclusions

The worsening of auto credit score availability has vital implications for each customers and business stakeholders. For customers, the tightening of credit score requirements has restricted entry to low charges for car financing. Naturally, that is making it harder to buy a brand new car in 2024, particularly for these with poor credit score.

For business stakeholders, together with dealerships and automakers, the tightening of credit score availability poses a big problem in driving car gross sales and sustaining market momentum. Analyzing the out there knowledge, the bottom conclusion one can draw is {that a} decline in credit score approval charges impacts gross sales volumes and profitability. This is especially damaging to dealerships that rely closely on OAC financing to ease the strain of the sale and facilitate the motion of each new and particularly used inventory.

In our view the answer that we expect will work finest is to discover various financing choices. This could embrace partnering with various lenders, or spreading the financing load throughout greater than a single lender to cut back total danger to every lender.

Some dealerships have additionally began providing versatile financing charges tied to the federal prime index (8.5% on the time of this writing), though that is principally getting used as a stopgap measure to maintain gross sales up. It has little viability for long run use, particularly with inflation creeping upwards because it has for the previous three years.

Naturally, dealerships and automakers are eager to deal with buyer retention and loyalty, so one other resolution could also be to supply incentives for accepting larger credit score rates of interest. These incentives may embrace offering all servicing lined for a number of years, or offering some choices for free of charge, as that value might be recovered within the elevated financing curiosity.

If these options don’t work, the one different resolution that presents itself is direct financial institution financing via a long-term mortgage with vital collateral comparable to house fairness. Nevertheless, the present pattern in auto credit score approvals appears to be like like it’s going to worsen earlier than it will get higher, so for some it merely comes right down to 2024 not being the yr to purchase a automobile.

Source: www.goodcarbadcar.internet