A poor credit rating could make getting a automobile mortgage harder – and enhance the price of that mortgage in the long term. But so long as you might be accountable about your mortgage, it may well finally show you how to enhance your credit score rating.

In this text, you’ll discover details about credit score scores and the way you should utilize an auto mortgage to assist construct or rebuild your rating. You’ll additionally discover some suggestions for extra methods to work on bringing your credit score rating up.

Auto Loans May Be an Opportunity For People With Bad Credit

One of the hardships for individuals with poor credit is the provision of credit score itself. Lenders could also be reluctant to supply credit score to individuals with low scores. This ends in a no-win scenario whereby individuals want credit score to enhance their scores, however can’t get credit score on account of their scores. Specifically, most lenders will contemplate a FICO credit score rating underneath 580 to be a “bad” credit score rating.

Auto loans, nonetheless, can typically be one of many simpler sorts of credit score to acquire for individuals with low scores. Car loans are secured loans that use the car as collateral, which means a lender can repossess the automobile if the borrower fails to make funds. This signifies that lenders have extra safety with auto loans than they do with different types of credit score corresponding to bank cards and private loans.

Eric Ridley, an lawyer who focuses on chapter and credit score points, instructed Automoblog that automobile loans will help individuals construct credit score in some circumstances.

“An auto loan may be a good option for someone with bad credit and few other credit options, as it provides the opportunity to rebuild your score,” says Ridley. “But auto loans are a two-edged sword.”

Bad Credit Car Loans Can Have Sky-High Interest Rates

One of the most important drawbacks with auto loans for individuals with poor credit is that they typically include excessive rates of interest. In basic, the decrease your credit score rating, the upper you rate of interest will seemingly be. Although legally the utmost rate of interest for an auto mortgage is 16%, some lenders manipulate the small print to cost annual share charges (APRs) as excessive as 25%.

“It’s not uncommon for lenders to charge extremely high interest rates to borrowers with poor or limited credit,” Ridley says. “This could cause not only the monthly payment, but the cost of the loan, to become unaffordable, and could result in pinched finances.”

Still, that doesn’t imply that you must rule out auto loans as a credit-building alternative completely, in response to Ridley. He says that even high-interest fee auto loans can nonetheless be helpful, however that debtors ought to be certain they perceive all the small print of their mortgage earlier than signing on.

“It’s critical to make sure you’re not ‘buying payments’ but that you understand and are comfortable with the terms of the loan, including the interest rate and any other associated costs, before entering into the agreement.”

Car Loans For People With Bad Credit Have Other Considerations

Borrowers produce other components to weigh past simply the monetary price of a high-interest fee auto mortgage. For instance, opening any line of credit score often has a short lived detrimental affect on an individual’s credit score rating. That means debtors ought to anticipate a dip of their rating earlier than they’ll construct it again up with common funds.

Ridley says that it’s additionally essential to think about the impact a brand new mortgage could have on a borrower’s credit score utilization ratio. This measures how a lot of an individual’s accessible credit score they’re presently utilizing. While some sorts of credit score enhance an individual’s accessible credit score and due to this fact decrease the ratio, that’s sometimes not the case with auto loans, Ridley says.

“If you take on a vehicle loan, you are immediately using 100% of the available credit on that credit line,” he says. “So, it’s important to get an auto loan in combination with other revolving credit, such as credit cards.”

How To Use a Bad Credit Car Loan To Build Credit

Building or rebuilding a credit score rating takes time and includes a couple of various factors. While an auto mortgage isn’t essentially the only finest device for bettering your rating, it may be an integral a part of a credit-building technique.

Get Pre-Approved

Pre-approval is the method of getting an authorized spending finances from a lender. To decide your finances, lenders verify your credit score historical past and different monetary data. This is called a “hard credit check.” Once you might be pre-approved for an auto mortgage, a lender will difficulty you a pre-approval verify that’s good for any quantity as much as your restrict. In different phrases, a pre-approval basically ensures a mortgage.

This is completely different from pre-qualification. While each processes offer you an thought of your finances, pre-qualification is just not a dedication from a lender. It makes use of self-reported data to provide an estimated finances in what’s generally known as a “soft credit check.” Soft credit score checks don’t affect your credit score rating. That means pre-qualification is an effective device that can assist you study what you may afford while you first begin in search of a automobile.

Since the exhausting credit score verify required for a pre-approval can have a detrimental affect in your credit score rating, and a pre-approval is just legitimate for a restricted time, you must wait to get pre-approved till you might be within the place to make a purchase order.

Stay Well Under Budget

It will be tempting to spend the utmost amount of cash you’re authorized for, however that’s sometimes not really useful. As lengthy because the automobile you wish to purchase meets your lender’s necessities, you may spend as little as you need.

Borrowing lower than you may afford leaves room in your finances for different issues that will come up. Even if you happen to don’t tackle any new bills, inflation can drive up the price of dwelling and go away you with much less expendable earnings than you had while you agreed to your auto mortgage. This could make it troublesome to satisfy funds.

Avoid “Buy Here, Pay Here” Dealerships

“Buy here, pay here” dealerships supply in-house financing choices for automobile consumers. These can appear to be a superb choice as a result of they could approve some consumers that different lenders received’t. However, that tends to come back at a price, in response to Ridley.

“These dealers sell used cars at high prices to desperate people and make a fortune on the high-interest loans they hold,” he says. “Some of them even want you to default so they can repossess the car and sell it again to someone else.”

Always Make Payments On Time

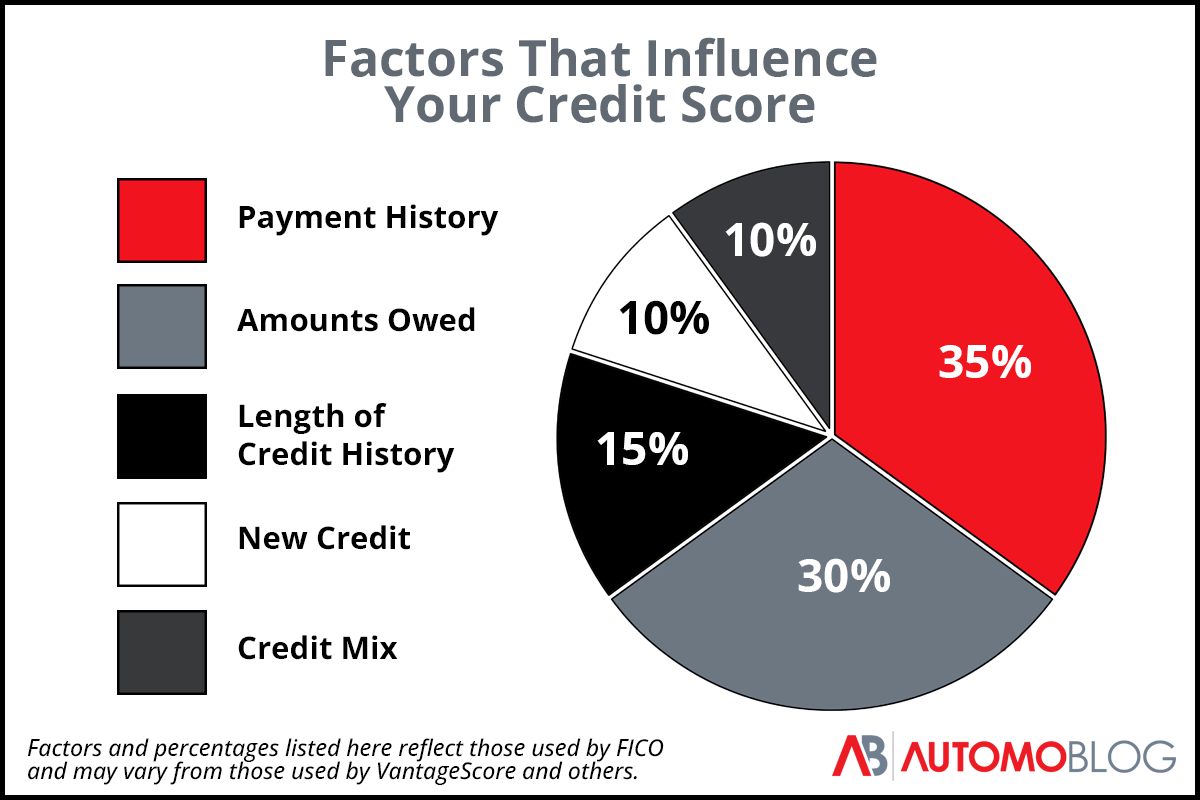

Your cost historical past is the only most influential think about your credit score historical past, accounting for 35% of your rating. That signifies that making your whole required funds on time is crucial to bettering your credit score rating. A single missed cost may erase months of progress.

Some lenders could also be prepared to work with you if you happen to get in contact earlier than your cost due date and allow them to know you received’t be capable to meet your obligations. They might be able to arrange a partial cost or discover different options.

However, not all lenders supply this, so it’s not an choice you must rely on. This is an effective motive to remain underneath your authorized finances.

Pay More When Possible

Many lenders provide the choice to pay extra in direction of your principal – or the remaining mortgage stability – after you’ve got met your month-to-month cost. Reducing your principal can lower the quantity you pay in curiosity, particularly early within the mortgage time period.

This additionally decreases your loan-to-value (LTV) ratio by decreasing your debt whereas growing the quantity of fairness you’ve got within the automobile. A decrease LTV ratio can, in flip, assist enhance your credit score rating.

Get Out From “Underwater” as Quickly as You Can

Owing extra in your automobile than it’s value is called being “underwater” or “upside down” on a mortgage. This is a harmful monetary place to be in, but when it’s important to tackle a poor credit automobile mortgage it could be unattainable to keep away from.

If you may afford to make additional funds, decreasing the principal in your mortgage till it’s lower than the worth of the car is nice apply. This can ultimately get you out from underwater and means that you can begin turning your debt into an asset.

Refinance Your Loan on the Right Time

Refinancing is the method of getting a brand new mortgage to repay your present mortgage. This will be an efficient device when the time is true to take action. If you’ve labored exhausting to enhance your credit score rating, you will have entry to decrease rates of interest than you probably did while you took on the unique mortgage.

However, it’s not at all times a superb time to refinance. Applying for a brand new mortgage will quickly decrease your rating. It additionally comes with one other spherical of charges that will exceed what you’d save with a brand new mortgage fee.

Most specialists suggest ready to refinance till you’ve seen a big enchancment in your rating or have vastly lowered your LTV ratio. Alternatively, you could wish to contemplate refinancing if rates of interest on the whole have gone down because you took in your unique mortgage.

Use Other Credit-Building Tools

As Ridley talked about, there are a number of different instruments that may show you how to construct or rebuild your credit score rating. Some of those could even be preferable to auto loans for that function.

Some of the instruments he recommends embody:

- Secured bank cards: These bank cards perform like “regular” bank cards however are backed by a deposit you make with the lender, often within the vary of $250 to $500. This deposit turns into your new credit score restrict.

- Credit builder loans: Some lenders supply small private loans particularly designed to assist individuals enhance their credit score.

- Authorized person standing: You can “piggyback” on a trusted good friend’s or relative’s credit score by changing into a licensed person on a number of of their accounts. As lengthy as this individual meets their funds, you’ll begin to see your credit score enhance. Most specialists suggest avoiding having precise entry to the bank card or different line of credit score to forestall negatively impacting the account holder’s rating.

- Rent reporting: Some corporations can report lease funds to credit score bureaus, which will help set up a superb cost historical past if you happen to at all times pay on time. Not all corporations can or will do that, and you will have to ask for this service.

Auto Loans Can Help Build Credit If You’re Responsible

An auto mortgage isn’t a magic bullet for bettering your credit score, however it may be one in all a number of instruments you should utilize to work in direction of a better rating. As you’re employed to enhance your credit score, understand that many lenders now supply free credit score experiences that can assist you preserve monitor of your rating. If yours doesn’t, you can even get one free credit score report from every of the three credit score reporting businesses as soon as per yr.

Ultimately, a automobile mortgage can solely show you how to construct credit score if you’re accountable about it. At the naked minimal, you’ll must just remember to can commit to creating month-to-month funds and to at all times doing so on time. While the method isn’t instant, if you happen to dependably meet your obligations and apply different good credit score habits, you must begin to see your rating enhance over time.

Source: www.automoblog.web